Texas Instruments (TXN): From the TI-83 to Powering the Future of Electronics 🔌 📱

As long as the world keeps demanding more chips, TI should be able to keep calculating strong returns for shareholders. And if all else fails, we’ll still have the TI-83 to fall back on.

Latest 10-K Filing | About StrataFinance | How to Read the Layers Chart

AI-written, human-approved. Read responsibly.

The Bottom Line Upfront 🧮

Texas Instruments (TI) is a semiconductor powerhouse that has been crunching numbers and powering electronics for over 90 years. With a strong focus on analog and embedded processing chips, TI has calculated a winning formula in the industrial and automotive markets. Despite fierce competition, the company’s manufacturing prowess, broad product portfolio, and direct customer relationships add up to a compelling long-term investment story. So grab your TI-83, and let’s dive into the numbers! 📊

Layer 1: The Business Model 🏭

TI designs and manufactures the building blocks of modern electronics - semiconductors. The company’s chips perform critical functions like converting real-world signals into digital data, managing power, and acting as the “brains” of electronic devices.

Analog Segment (78% of Revenue) - Makes chips that interface with the physical world - Manages power in electronic equipment - Includes power management and signal chain products

Embedded Processing Segment (16% of Revenue) - Produces microcontrollers and processors optimized for specific tasks - Customers invest heavily in software for these chips, creating sticky relationships

Other segment (6% of revenue)- that includes things like the iconic TI-83 calculators that haunted your high school math classes. 😱 Believe it or not, they still make them!

Internally, TI is laser-focused on growing free cash flow per share over the long haul. The company owns and operates most of its manufacturing capacity, providing cost advantages and control over its supply chain.

Layer 2: Category Position 🥊

The analog and embedded processing markets are highly fragmented, with TI duking it out with dozens of competitors. These include companies like: Analog Devices, Microchip Technology, STMicroelectronics, & NXP Semiconductors.

TI’s secret weapons are:

Manufacturing scale and technology leadership 💪

Broad product portfolio with ~80,000 chips 🎰

Direct customer relationships through TI.com 💻

Strong positions in industrial and automotive markets 🏭🚗

The company has made a strategic bet on the industrial and automotive markets, which represent a combined 74% of revenue. These markets offer the best mix of growth, profitability, and longevity. So far, that bet seems to be paying off.

Layer 3: The Top Line 📈

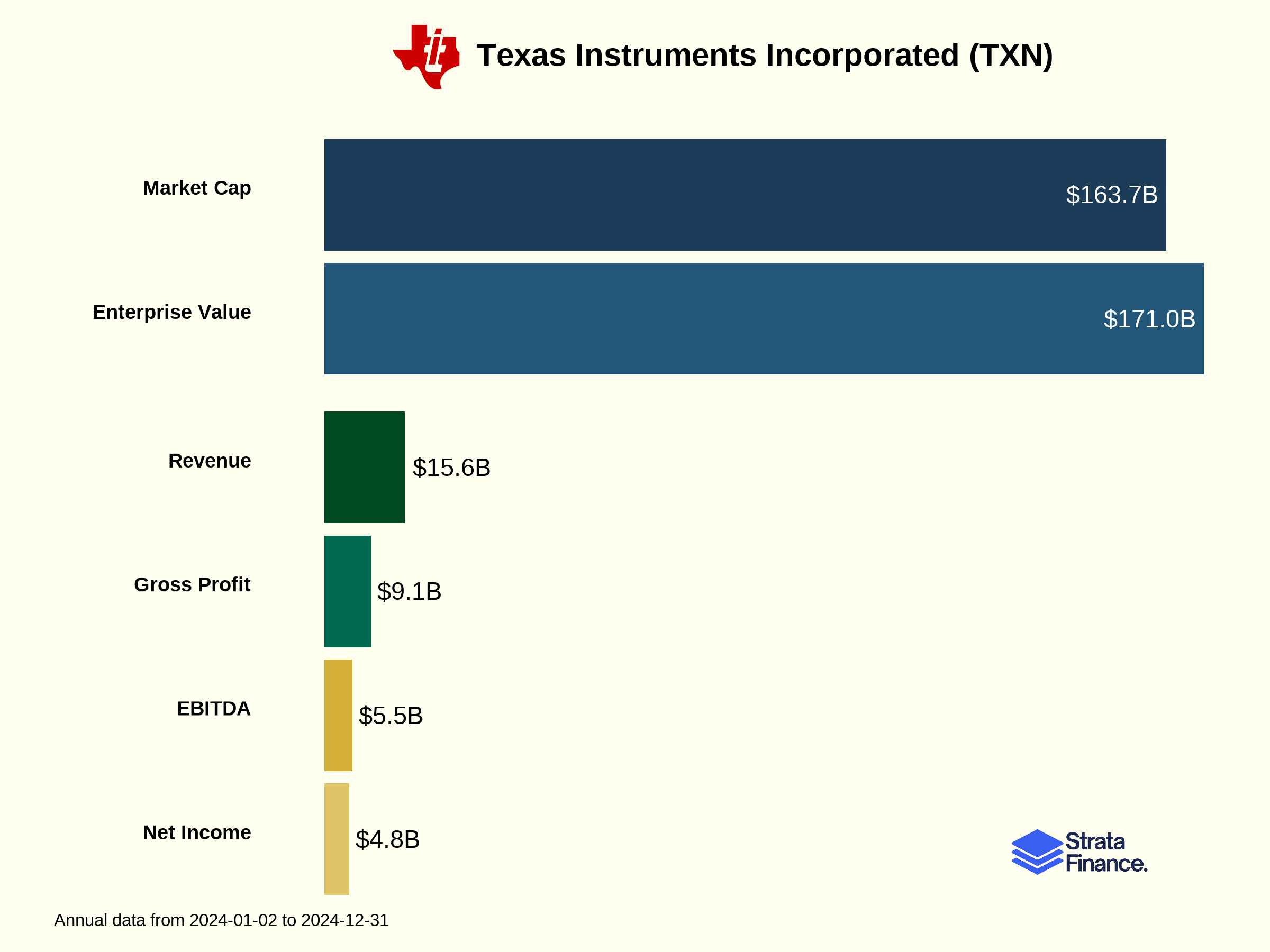

In 2024, TI raked in $15.641 billion in revenue. Here’s how that breaks down:

Revenue by End Market:

Industrial: 40%

Automotive: 34%

Personal Electronics: 15%

Communications Equipment: 5%

Enterprise Systems: 4%

Calculators & other products: 2%

Geographic Revenue:

United States: 33%

China: 19%

Europe: 26%

Japan: 10%

Rest of Asia: 10%

Rest of World: 2%

TI has a diverse customer base, with no single customer accounting for more than 10% of sales. Over 40% of revenue comes from outside the top 100 customers.

However, total revenue declined 10.7% in 2024, driven by weakness in the analog segment (↘️ 15%). Embedded processing grew slightly (↗️ 3%), while the “Other” segment declined (↘️ 21%). Looks like even TI isn’t immune to the ups and downs of the semiconductor cycle. 🎢

Layer 4: Cash is King 👑

Despite the revenue headwinds, TI is still minting money. In 2024, the company generated:

Gross Margin: 58.1%

Operating Margin: 34.9%

Free Cash Flow: $1.5 billion (9.6% of revenue)

However, margins did compress in 2024, with gross margin down from 63% and operating margin down from 42% in the prior year. The main culprits? Lower revenue and higher manufacturing costs related to capacity expansion.

TI’s cost structure is dominated by fixed costs due to its in-house manufacturing model. The company plows significant money into R&D ($1.96 billion in 2024) and capital expenditures ($4.8 billion in 2024) to stay on the cutting edge.

When it comes to capital allocation, TI prioritizes:

Organic growth investments

Dividends

Share repurchases

Selective acquisitions

With $7.58 billion of cash on the balance sheet, TI has plenty of dry powder to fund these priorities and weather any short-term storms. The company generated $6.32 billion in operating cash flow in 2024, so paying the bills isn’t an issue.

Layer 6: By your Powers Combined 🦸♂️

Let’s see how TI stacks up on Helmer’s Seven Powers:

Scale Economics: ✅

TI’s 300mm wafer manufacturing provides a 40% cost advantage over 200mm wafers

Large manufacturing footprint creates economies of scale

Switching Costs: ✅

Customers invest significant time and money into software for TI’s embedded processors

High switching costs once a customer has designed a TI chip into their product

Network Effects: ❌

No major network effects in the semiconductor manufacturing game

Branding: ✅

Strong reputation for quality and reliability, especially in industrial and automotive

Iconic TI-83 calculator brand (for the high school nostalgia factor)

Counter Positioning: ✅

Vertically integrated manufacturing model sets TI apart from “fabless” competitors

Direct sales through TI.com provide an alternative to traditional distribution channels

Process Power: ✅

Advanced manufacturing capabilities on leading-edge process nodes

Streamlined product development engine churns out new chip designs

Cornered Resource: ❌

No truly unique patents or resources that competitors can’t replicate or design around

Layer 7: But you don’t have to take my word for it 🌈

The bull case for TI rests on a few key beliefs:

Semiconductor content in industrial and automotive applications will continue to grow rapidly 📈

TI’s manufacturing investments will provide sustainable cost and scale advantages 🏭

Direct customer relationships through TI.com will deepen competitive moats 🏰

The focus on free cash flow per share will drive long-term value creation 💰

Bears will point to risks like:

The inherent cyclicality of the semiconductor industry 🎢

Intensifying competition, especially from low-cost Asian manufacturers 👹

Potential execution missteps on the ambitious manufacturing capacity expansion plans 😅

Geopolitical tensions that could disrupt global trade flows 🌍

At the end of the day, TI’s long-term success hinges on its ability to ride the secular growth in semiconductor demand while maintaining its competitive advantages in manufacturing and customer relationships. With a 90+ year track record of innovation, the company has shown it can adapt to changing industry dynamics.

The significant investments in capacity expansion suggest management is confident in the long-term growth trajectory. As long as the world keeps demanding more and more chips, TI should be able to keep calculating strong returns for shareholders. And if all else fails, at least we’ll still have the TI-83 to fall back on! 🧮

Disclaimer: This guide is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. The information contained in this report has been obtained from sources believed to be reliable, but StrataFinance does not guarantee its accuracy, completeness, or timeliness.