JetBlue: The Struggling Middle-Seat Airline

SEC Filing: 10-K (2024) | About StrataFinance | How to Read the Layers Chart

AI-written, human-approved. Read responsibly.

The Bottom Line Upfront

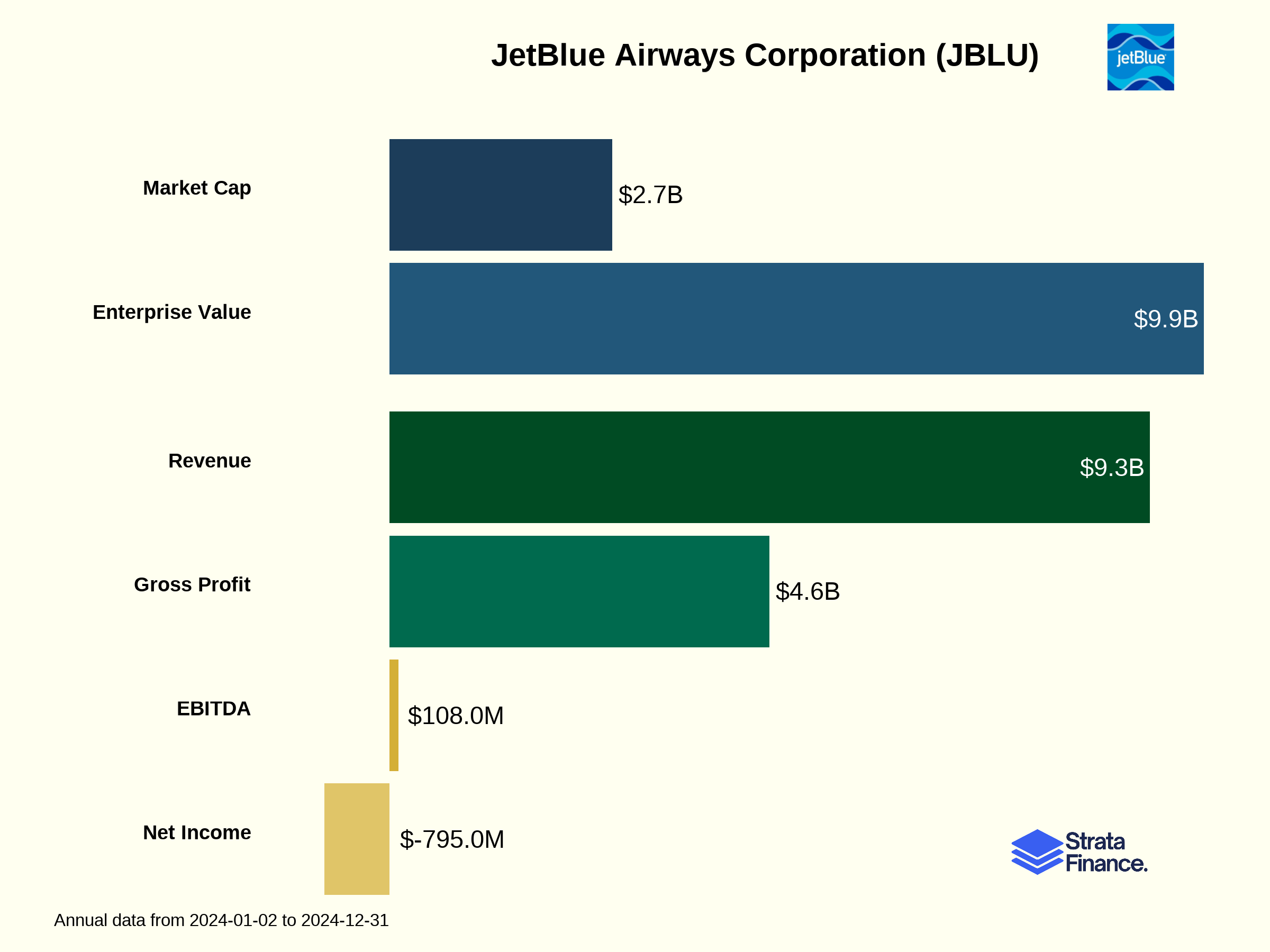

JetBlue Airways occupies a challenging middle position in the U.S. airline industry - offering better service than ultra-low-cost carriers but without the global network of legacy airlines. Despite strong brand recognition and loyal customers, JetBlue is currently unprofitable with a $795 million net loss in 2024 (including a $532 million Spirit merger write-off). The airline faces significant headwinds including engine issues, high debt levels, and intense competition in its Northeast-focused network. While its "JetForward" strategy and premium offerings like Mint® show promise, investors should approach with caution until the company demonstrates it can control costs and return to profitability.

Layer 1: The Business Model 🏛️

The JetBlue Experience ✈️

JetBlue Airways is "New York's Hometown Airline®," but don't let that fool you into thinking they're just a regional player. Founded in 1998 and taking flight in 2000, JetBlue has built its business around a simple premise: what if flying didn't have to suck?

At its core, JetBlue sells air transportation with a twist – they actually try to make it pleasant. Imagine that! While most airlines seem to be in a race to see how many passengers they can cram into a metal tube while charging for everything short of breathing, JetBlue has zigged where others zagged.

Their business model revolves around three tiers of service:

Core Experience: The basic JetBlue offering that's already better than most competitors' standard service. All passengers get free carry-on bags, complimentary seatback entertainment, free high-speed Wi-Fi (Fly-Fi®), and free snacks and non-alcoholic beverages. Within this tier, customers can choose from four fare options: Blue Basic, Blue, Blue Plus, and Blue Extra. It's like a buffet of options where even the cheapest plate still comes with decent food.

EvenMore®: Recently rebranded from EvenMore® Space in January 2025, this tier offers additional legroom, priority security access, early boarding, dedicated overhead bin space, complimentary alcoholic beverages, and premium snack options. Basically, it's for people who want to feel slightly less like sardines.

Mint®: JetBlue's premium service available on select coast-to-coast, Caribbean, Latin American, and all transatlantic routes. Mint® features lie-flat beds with Tuft & Needle® sleep experience, premium dining options, and enhanced amenities. On select routes, they offer an upgraded Mint® experience with private suites. This is for people who want to arrive at their destination without feeling like they've been folded into origami.

Network Strategy 🗺️

JetBlue operates a predominantly point-to-point system focused on six key cities: New York, Boston, Fort Lauderdale-Hollywood, Orlando, Los Angeles, and San Juan. About 96% of their routes touch at least one of these focus cities. Think of it as a starfish rather than a wheel-and-spoke design used by legacy carriers.

As of December 31, 2024, JetBlue served over 100 destinations across the United States, Caribbean, Latin America, Canada, and Europe with a fleet of 290 aircraft, primarily Airbus A220, A320, and A321 models, along with some remaining Embraer E190 aircraft that are being phased out. Their fleet's average age is 12 years – practically adolescent in airline years.

Beyond Just Flights 🏝️

JetBlue has expanded beyond just flying planes:

JetBlue Travel Products (JBTP): A wholly-owned subsidiary offering vacation packages through JetBlue Vacations® and Paisly® by JetBlue. Think of it as JetBlue saying, "Hey, since you trust us to fly you there, why not let us book your hotel and rental car too?"

TrueBlue® Loyalty Program: Their frequent flyer program allows members to earn points through JetBlue flights and partners. Points can be redeemed for flights with no blackout dates. The program includes TrueBlue Mosaic® status with four tier levels offering additional perks for their most loyal customers.

JetBlue Ventures: A wholly-owned subsidiary that invests in early-stage startups focused on improving travel. It's like JetBlue's version of a venture capital fund, but with a focus on companies that might eventually help their core business.

Key Success Metrics 📊

JetBlue measures success through several key operational metrics:

Available Seat Miles (ASMs): The number of seats available for passengers multiplied by the miles the seats are flown (66.1 billion in 2024 ↘️)

Revenue Passenger Miles (RPMs): The number of miles flown by revenue passengers (55.0 billion in 2024 ↘️)

Load Factor: The percentage of available seats filled with passengers (83.2% in 2024 ↗️)

Yield: Average fare per mile (15.68 cents in 2024 ↘️)

On-time Performance: Percentage of flights arriving within 14 minutes of scheduled time (74.1% in 2024 ↗️)

Completion Factor: Percentage of scheduled flights completed (98.6% in 2024 ↗️)

Layer 2: Category Position 🏆

The Airline Pecking Order 🦅

In the U.S. airline industry, JetBlue occupies a unique middle position. They're not a bare-bones, "we'll charge you for oxygen" ultra-low-cost carrier like Spirit or Frontier, nor are they a legacy behemoth like American, Delta, or United with extensive international networks and business class offerings.

JetBlue is what you might call a "high-value" low-cost carrier – offering more amenities than budget airlines while maintaining lower costs than the legacy carriers. It's like being the Target in an industry of Walmarts and Nordstroms.

Their major competitors include:

Market Share and Geographic Strength 🌎

JetBlue's market presence is strongest in the Northeast corridor of the U.S., particularly in the New York and Boston metropolitan areas. Their seat share by focus city tells the story:

Boston: 25% (their strongest position)

San Juan: 26%

Fort Lauderdale: 19%

New York metro area: 14%

Orlando: 10%

Los Angeles: 3%

This concentration gives them strength in key markets but also creates vulnerability to regional disruptions. It's like having all your eggs in a few very congested, weather-prone baskets.

Recent Wins and Challenges 🏆

Wins:

Improved operational performance, with on-time performance increasing to 74.1% in 2024 from 67.4% in 2023

Successful launch of transatlantic service to Europe, with capacity growing to 5.3% of their network

Enhanced premium offerings with plans for airport lounges at JFK and Boston Logan

Announced plans for a new domestic first-class cabin on non-Mint® aircraft beginning in 2026

Challenges:

Termination of the Spirit Airlines merger in March 2024, resulting in a $532 million write-off

Engine issues with Pratt & Whitney powerplants, with 11 aircraft grounded in 2024 and expectations of mid-to-high teens aircraft out of service in 2025

Continued net losses and negative operating margins

Intense competition in core markets

Competitive Advantages and Disadvantages 🔄

Advantages:

Strong brand recognition and customer loyalty

Premium amenities included in base fares (free Wi-Fi, entertainment, snacks)

Strategic positions in high-value geographic markets

TrueBlue® loyalty program driving repeat business

Disadvantages:

Heavy dependence on congested Northeast airspace

Higher cost structure than ultra-low-cost carriers

Limited international network compared to legacy carriers

Vulnerability to weather disruptions in key markets

Layer 3: Show Me The Money! 📈

Revenue Breakdown 💵

JetBlue generated $9.3 billion in total operating revenue in 2024 ↘️, a 3.5% decrease from 2023. This revenue comes from two primary sources:

Passenger Revenue: $8.6 billion (92.9% of total) ↘️

Ticket sales

Baggage fees

Ancillary products like EvenMore®

Other Revenue: $662 million (7.1% of total) ↗️

TrueBlue® loyalty program non-transportation revenue

Vacation packages

Airport concessions and advertising

Geographically, JetBlue's 2024 revenue was distributed across:

Domestic & Canada: $5.64 billion (60.8%)

Caribbean & Latin America: $3.17 billion (34.2%)

Atlantic (European routes): $470 million (5.0%)

Customer Mix and Purchasing Patterns 👨👩👧👦

JetBlue focuses on three main customer segments:

Leisure travelers: Vacation-goers heading to beach destinations in Florida, the Caribbean, and Latin America

VFR (Visiting Friends and Relatives) travelers: People traveling to see family, who tend to be less seasonal and less affected by economic downturns

Business travelers: A smaller but growing segment, particularly in Boston and New York

The airline has been working to attract more business travelers with enhanced Mint® offerings and the planned introduction of domestic first class, but leisure and VFR travelers remain their bread and butter.

Key revenue metrics for 2024 include:

Average fare: $212.78 ↗️ (up 0.5% from 2023)

Yield per passenger mile: 15.68 cents ↘️ (down 1.5%)

Passenger revenue per ASM: 13.04 cents ↘️ (down 0.8%)

Operating revenue per ASM: 14.04 cents (flat)

Growth Drivers and Headwinds 🌬️

Growth Drivers:

Premium product offerings: Mint®, EvenMore®, and the planned domestic first class

TrueBlue® loyalty program: Generated $634 million in air transportation revenue ↗️ and $464 million in non-transportation revenue ↗️

Transatlantic expansion: European routes growing as a percentage of capacity

JetBlue Travel Products: Vacation packages showing growth

Headwinds:

Capacity constraints: 3.5% reduction in capacity in 2024 due to aircraft groundings and network optimization

Engine issues: Pratt & Whitney problems affecting fleet availability

Competitive pressure: Intense competition in core markets

Operational challenges: Northeast airspace congestion and weather disruptions

Seasonality Factors 🌞❄️

JetBlue's business has natural seasonality patterns:

Peak periods: Caribbean and Latin American routes are strongest in winter months (October-April)

Western routes: Strongest during summer months

Northeast routes: Subject to weather disruptions in winter

VFR traffic: Helps smooth out some seasonality effects

The airline actively manages this mix to reduce the impact of seasonality, but it remains a factor in quarterly performance variations.

Layer 4: Cash Rules Everything Around Me 💰

Profitability Picture 📉

Let's be blunt: JetBlue isn't profitable right now. The airline reported a net loss of $795 million for 2024 ↘️, compared to a net loss of $310 million in 2023. That's not great, but there's context needed – $532 million of that loss came from writing off Spirit-related costs after their merger fell apart.

Operating metrics tell a similar story:

Operating loss: $684 million ↘️

Operating margin: -7.4% ↘️ (worsened from -2.4% in 2023)

Loss per share: $2.30 ↘️ (worsened from $0.93 in 2023)

Excluding special items (like the Spirit write-off), JetBlue's adjusted figures look somewhat better:

Adjusted operating loss: $93 million ↘️

Adjusted operating margin: -1.0% ↘️

Adjusted loss per share: $0.71 ↘️

Still not profitable, but less dire than the headline numbers suggest.

Cost Structure Breakdown 💸

JetBlue's operating expenses totaled $10.0 billion in 2024 ↗️, a 1.2% increase from 2023. Major expense categories included:

Salaries, Wages and Benefits: $3.26 billion (32.8% of expenses) ↗️

Up 6.8% from 2023 due to wage increases, especially from the pilot union contract

Aircraft Fuel: $2.34 billion (23.5% of expenses) ↘️

Down 16.5% from 2023 due to lower fuel prices ($2.75 per gallon, down 12.1%) and reduced consumption

Landing Fees and Other Rents: $659 million (6.6% of expenses) ↗️

Depreciation and Amortization: $655 million (6.6% of expenses) ↗️

Maintenance, Materials and Repairs: $628 million (6.3% of expenses) ↘️

Special Items: $591 million (5.9% of expenses) ↗️

Includes $532 million in Spirit-related costs

Cost per available seat mile (CASM) increased by 4.9% to 15.08 cents ↗️. Excluding fuel and special items, CASM ex-fuel increased by 6.6% to 10.55 cents ↗️. This isn't a great trend – costs are rising faster than revenue, which is a recipe for continued losses.

Balance Sheet Health 💉

As of December 31, 2024, JetBlue had:

Liquidity: $3.9 billion (cash, investments, and marketable securities)

Total debt and finance lease obligations: $8.6 billion

Current maturities: $392 million

Long-term debt and finance lease obligations: $8.1 billion

The airline completed several significant financing transactions in 2024:

Raised $2.8 billion through TrueBlue® Financings (secured by loyalty program assets)

Issued $460 million of 2.50% convertible senior notes

Secured $662 million in floating rate equipment notes

Entered into $668 million of failed sale-leaseback transactions

JetBlue also deferred approximately $3.0 billion in capital expenditures by pushing 44 Airbus A321neo deliveries from 2025-2029 to 2030 and beyond. This helps near-term liquidity but means they'll have older aircraft for longer.

Capital Allocation Priorities 🎯

JetBlue's current capital allocation priorities are:

Maintaining liquidity: Ensuring sufficient cash reserves to weather continued challenges

Fleet modernization: Investing in fuel-efficient aircraft while deferring some deliveries

Product enhancements: Airport lounges, domestic first class, and other customer experience improvements

Debt management: Refinancing and restructuring debt to manage maturities

The airline is not currently paying dividends or repurchasing shares, focusing instead on returning to profitability and strengthening the balance sheet.

Layer 5: What Do We Have to Believe? 📚

The Bull Case 🐂

For JetBlue to succeed long-term, investors need to believe:

JetForward strategy will work: The four-pronged approach (reliable service, East Coast leisure network, valued products, secure financial future) will drive improved performance.

Premium offerings will drive revenue growth: Mint®, EvenMore®, and the planned domestic first class will attract higher-paying customers and improve yields.

Cost control initiatives will succeed: JetBlue can manage rising labor and maintenance costs while improving operational efficiency.

Network optimization will pay off: Focusing on high-performing routes and exiting underperforming markets will improve profitability.

Engine issues are temporary: Pratt & Whitney problems will be resolved without long-term fleet implications.

Leisure travel demand remains strong: Post-pandemic travel patterns will continue to favor JetBlue's leisure-focused network.

The Bear Case 🐻

Skeptics would point to:

Structural cost disadvantages: JetBlue's cost structure is higher than ultra-low-cost carriers but without the revenue premium of legacy carriers.

Geographic concentration risk: Heavy dependence on the congested Northeast corridor creates vulnerability to disruptions.

Continued losses: The airline hasn't demonstrated consistent profitability, even excluding special items.

Fleet challenges: Engine issues and deferred deliveries could lead to an aging, less efficient fleet.

Competitive pressure: Legacy carriers and ultra-low-cost carriers continue to squeeze JetBlue from both ends of the market.

Debt burden: High debt levels could limit financial flexibility if conditions worsen.

Key Metrics to Watch 👀

Investors should monitor:

Operating margin: Can JetBlue return to positive territory?

CASM ex-fuel: Are cost control efforts working?

Yield and RASM: Is revenue quality improving?

Load factor: Are planes flying full?

On-time performance and completion factor: Is operational reliability improving?

Aircraft utilization: Are they efficiently using their fleet?

Liquidity and debt levels: Is the balance sheet strengthening?

The Bottom Line 📝

JetBlue Airways occupies an interesting middle position in the U.S. airline industry – better service than ultra-low-cost carriers but lower costs than legacy airlines. This differentiation has built a loyal customer base, but hasn't translated to consistent profitability.

The JetForward strategy makes sense on paper, focusing on core strengths and addressing key weaknesses. However, execution will be challenging in an industry known for thin margins and vulnerability to external factors.

For investors, JetBlue represents a turnaround story with potential upside if management can successfully execute their strategy. However, the continued losses, high debt levels, and operational challenges suggest caution is warranted.

The airline industry has never been for the faint of heart, and JetBlue is no exception. As Warren Buffett once quipped before he ironically invested in airlines himself, "If a farsighted capitalist had been present at Kitty Hawk, he would have done his successors a huge favor by shooting Orville down." JetBlue might prove that sentiment wrong, but they've got some turbulence to navigate first.

Disclaimer: This guide is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. The information contained in this report has been obtained from sources believed to be reliable, but StrataFinance does not guarantee its accuracy, completeness, or timeliness.